Source: World Trade Organization – WTO (video statements)

Director-General Ngozi Okonjo-Iweala welcomed Mary Ng, Canada’s Minister of Export Promotion, International Trade and Economic Development, to the WTO on 7 February. During their meeting, they discussed Canada’s strong commitment to multilateral trade and the importance of a rules-based trading system in supporting businesses and workers.

Download this video from the WTO website:

https://www.wto.org/english/res_e/webcas_e/webcas_e.htm

January 2025 was the hottest on record – a whole 1.7°C above pre-industrial levels. If many climate-watchers expected the world to cool slightly this year thanks to the natural “La Niña” phenomena, the climate itself didn’t seem to get the memo. In fact, January 2025’s record heat highlights how human-driven ocean warming is increasingly overwhelming these natural climate patterns.

La Niña is a part of the El Niño southern oscillation, a climate fluctuation that slowly sloshes vast bodies of water and heat between different ocean basins and disrupts weather patterns around the world. El Niño was first identified and christened by Peruvian fishermen who noticed a dismal drop in their catch of sardines that coincided with much warmer than usual coastal waters.

El Niño is now well known to be part of a grander climate reorganisation that also has a reverse cool phase, La Niña. As vast swathes of the eastern Pacific cool down during La Niña, this has knock on effects for atmospheric weather patterns, shifting the most vigorous storms from the central Pacific to the west and disrupting the prevailing winds across the globe.

This atmospheric reaction also helps to amplify the sea surface temperature changes. Typically, La Niña will lower the global temperature by a couple of tenths of a degree Celsius.

In 2024 the Pacific swung from moderate El Niño conditions to a weak La Niña. However, this time around, it’s apparently not enough to stop the world warming – even temporarily. So what’s different this time?

Each La Niña cycle is unique

Scientists aren’t entirely surprised. Each El Niño and La Niña cycle is unique. Following an surprisingly lengthy “triple dip” La Niña starting in 2020, the El Niño that developed in 2023 was also unusual, struggling to stand out against globally warm seas. The switch to a weak La Niña has only slightly cooled a narrow band along the equatorial Pacific, while surrounding waters have remained unusually hot.

Recent research shows human caused warming of the ocean is accelerating – so a year on year rise in temperature is itself getting bigger – and this is dominating to an ever greater extent over El Niño and other natural oscillations in the climate. This means that even during La Niña – when equatorial eastern Pacific waters are cooler than normal – the rest of the world’s oceans have remained remarkably warm.

More carbon, less reflection

There is also a sense of inevitability as greenhouse gas levels continue to grow, even despite the demise of El Niño. During El Niño years, the land tends to absorb less carbon from the atmosphere as large continental areas, such as parts of South America, temporarily dry out causing less plant growth and more carbon-emitting plant decay.

La Niña tends to have the opposite effect. In the strong La Niña of 2011, so much extra rain fell on the normally dry lands of Australia and parts of South America and southeast Asia that sea levels dropped as the land held on to this excess moisture borrowed temporarily from the ocean. This meant more carbon was taken from the atmosphere to feed extra plant growth. But despite the switch to La Niña, the rate of rise in atmospheric carbon in 2024 and January 2025 remains above the already high levels of previous years.

To this we can also add the diminishing effects of particle pollution from industry, big ships and other sources of “aerosols”, which in some regions had added a reflective haze in the atmosphere meaning the world absorbed less sunlight. Clean air policies introduced over time have made the world less smoggy, but they also seem to have caused clouds to reflect less sunlight back to space, adding to global heating.

As industrial activity continues to spew greenhouse gases into the air, while air cleansed of particle pollution causes more sunlight to reach the ground, this growing heating effect is beginning to drown out natural fluctuations, tipping the balance toward record warmth and worsening hot, dry and wet extremes.

The long-term trend is clear

But, just as one swallow doesn’t make a summer, a single month is not reflective of the overall trajectory of climate change. Changing weather patterns from week to week can rapidly shift temperatures especially over big landmasses, which warm up and cool down more quickly than the oceans (it takes a long time to boil up water for your vegetables but not long to super heat an empty pan).

Large areas of Europe, Canada and Siberia experienced much less cold weather than is normal for January (by up to about 7°C). Parts of South America, Africa, Australia and Antarctica also experienced above average temperatures. Along with the balmy oceans, this all contributed to an unexpectedly warm start to 2025.

While this particular warm January isn’t necessarily cause for immediate alarm, it suggests natural cooling phases may become less effective at temporarily offsetting the impact of rising greenhouse gas levels on global temperatures. And to limit the scale of the inevitable, ensuing climate change, there is a clear, urgent need to rapidly and massively cut greenhouse gas emissions and to properly account for the true cost of our lifestyles on societies and the ecosystems that underpin them.

Don’t have time to read about climate change as much as you’d like?

Richard P. Allan does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

Drivers are reminded of traffic-pattern changes on Highway 99 at Steveston Highway over three weekends, beginning tonight, Friday, Feb. 7, 2025.

These changes are necessary as crews dismantle and remove the old Steveston Highway crossing.

Highway 99 will be closed in both directions overnight Friday, Saturday and Sunday from 9 p.m. until 8 a.m. (until 5 a.m. on Monday). During these overnight closures, Highway 99 travellers will detour using the highway on/off ramps.

From 8 a.m. until 9 p.m. Saturday and Sunday, Highway 99 will be open with two lanes in each direction. However, lanes may be shifted to allow crews and heavy equipment to dismantle and remove the old structure. Drivers are asked to use caution through any detours and obey the construction zone speed limit.

The traffic-pattern changes will also be in effect over the weekends of Feb. 21-24 and Feb. 28-March 3. There will be no impact to traffic during the week or over the Family Day long weekend.

During these weekend overnight lane closures and daytime traffic-pattern changes, drivers can expect delays and should consider an alternative route. Check DriveBC for updates: https://www.drivebc.ca/

Details about the traffic-pattern changes can be found here: https://www.highway99tunnel.ca/current-work/

The Lucy Letby case is the latest in a number of UK criminal medical cases that, beyond the rights and wrongs of each verdict, raise serious questions around how such cases are tried – especially when the evidence is limited, complex, and circumstantial. These cases often rely heavily on expert witnesses, whose testimony is crucial yet can be open to interpretation.

As an expert in the intersection of criminal and medical law, I am particularly concerned with how prosecution teams gather expert evidence in such cases – and how it is then communicated to juries through expert witnesses.

Generally speaking, in complex medical cases, police and prosecutors may risk becoming overly reliant on a small pool of experts when dealing with highly technical issues beyond their expertise. This dependence can inadvertently lead to “cherry-picking” – selectively presenting evidence that supports a particular narrative, while overlooking alternative perspectives that could provide a more comprehensive or balanced view.

In the Letby case, the prosecution’s selection and interpretation of evidence has now been challenged by an independent panel of 14 neonatal and paediatric experts. Letby is serving 15 whole-life prison terms after being convicted of murdering seven babies and attempting to kill another seven at the Countess of Chester hospital in north-west England. The chair of the panel, retired Canadian neonatologist Dr Shoo Lee, was co-author of a 1989 academic paper on air embolism in babies that was used in the prosecution’s case, but now says this evidence was misinterpreted by the prosecution.

In complex medical cases, I’m concerned that prosecutors – who may lack the medical expertise needed to fully grasp these complexities – may gravitate toward experts whose opinions align with a prosecutorial narrative, whether consciously or not. This can result in a narrowing of expert perspectives which might tend to focus only on those that bolster the case for conviction, while alternative views that could provide a more balanced assessment are excluded or marginalised.

In trials where juries hear only a limited number of expert voices, there’s a risk they may not receive a sufficiently balanced understanding of the case. In addition, rare diagnoses may lack the robust scientific literature typically needed to validate medical opinions in court.

Medical experts, like professionals in any field, can have differing opinions, especially in cases involving judgment calls or grey areas in medical practice. Without exposure to a range of viewpoints, jurors may miss alternative interpretations of the same evidence, which could be crucial for fair deliberation.

Of course, the defence also has the opportunity to call its own experts, potentially offering counter-arguments to prosecution evidence. But decisions by a defence team not to call certain experts may be based on legal strategy, resource constraints, or concerns about how the testimony will withstand cross-examination. When this happens, it can amplify the weight of the prosecution’s selected experts, potentially skewing the jury’s understanding.

Jurors naturally place a high level of trust in experts, assuming their testimony is both accurate and confined to their area of expertise. So, when experts venture beyond their remit, jurors may accept these statements uncritically, unaware that such testimony may lack the depth required in such complex medical cases. This issue is particularly concerning in circumstantial prosecutions where the case often hinges more on expert interpretation than on direct evidence, increasing the risk of misunderstanding or misjudgment.

Expert overreach

Testimony from experts unfamiliar with the practical pressures of certain clinical settings may lead to distorted interpretations of what a “reasonable” course of action would have been under the circumstances. This can result in unfair judgments, particularly when the nuances of clinical decision-making aren’t fully explored.

Experts also sometimes “overreach” their duties in court, offering opinions that extend beyond their remit. In the case of surgeon David Sellu, who was jailed for gross negligence manslaughter in November 2013 before being freed three years later, having spent 15 months in prison, the court of appeal noted that expert witnesses had repeatedly expressed opinions on whether Sellu’s conduct amounted to gross negligence – an assessment the court said should have been left to the jury.

In that case, the experts directly addressed the “ultimate issue” of whether Sellu’s actions were grossly negligent. But that was for the jury to decide, not the experts, and I believe the trial judge should have intervened. A key change needed by the UK legal system, in my view, is to establish clearer guidelines to ensure experts do not exceed their role – whether in a complex financial fraud or criminal medical trial.

Incidentally, while the judge in the Sellu trial didn’t give the jury correct direction (this was a key finding by the court of appeal that made the conviction unsafe), I don’t think it was entirely the judge’s fault. The law surrounding gross negligence manslaughter, particularly when applied to doctors unintentionally causing a patient’s death, is fraught with ambiguity. The lack of clear guidelines on what constitutes “gross” negligence, coupled with inconsistent application of the law, has sparked widespread concerns about its fairness and appropriateness in the medical context..

Make-up of a jury

Letby’s trial also highlights the limitations of the current jury system in such complex medical cases. The original trial was one of the longest in UK legal history, lasting ten months. The idea of jury trials is you’re tried by your peers, but if you’re a healthcare professional, you’re arguably not really being tried by your peers.

In England, jury service is compulsory and jurors are chosen randomly from the electoral register, but there are some exemptions and deferrals available in specific circumstances, such as serious illness, disability, or full-time caregiving. Additionally, people can apply for deferral if serving would cause significant hardship due to work commitments, including shift work or conflicts with important public duties. This is particularly relevant for professionals who cannot easily take extended time away from their roles.

This adds to the question of whether a jury, composed of 12 lay people with no specialised medical knowledge, can effectively assess intricate, often conflicting medical evidence. As Rebecca Helm highlights in her book How Juries Work (2024), while expert testimony aims to enhance jury understanding of complex evidence, jurors often lack the necessary background knowledge to fully grasp or critically assess it. This can lead to challenges in properly weighing competing expert opinions, especially in adversarial systems where experts present differing views.

In the Letby case, the vast amount of medical evidence presented for each baby likely made it challenging for a lay jury to fully comprehend. Additionally, they may have felt intimidated or hesitant to ask the judge questions, further complicating their ability to critically engage with the evidence.

Of course, it’s important to understand the backdrop for cases like this. I’m very aware of how overstretched, understaffed and under-resourced our hospitals are. And in the Letby case, we know that severely premature babies who are born on the cusp of viability often have a lot of comorbidities. It’s vital that jurors have a clear understanding of such specific context – which is outside the normal experience of most of us – when they come to make their decisions.

The jury’s role is to assess expert evidence independently, yet this can be difficult without clear guidance. In the Sellu trial, the absence of a “route to verdict” document was another significant issue. While not always mandatory, such a document is often used in complex cases to help jurors separate medical facts from legal conclusions.

Without it, the jury was left without clear guidance, increasing the risk of confusion and misapplication of the law. While the court of appeal did not say a route to verdict was strictly required, it strongly indicated that its omission contributed to an unfair trial process.

Expert advisors for juries

In complex criminal cases, like fraud or medical trials, where a large amount of expert evidence is presented, it can be challenging for lay jurors to fully understand and assess the evidence. Elsewhere in Europe – including in Italy, Spain and France – expert judges or advisers are often involved in complex cases to help guide the jury and clarify professional standards relevant to the case.

Given the complexity of cases like Sellu and Letby, it’s worth considering whether jury reform is needed in the UK to ensure fair trials. A potential solution is the inclusion of an expert, such as a medico-legal advisor, who can assist juries in understanding and weighing medical evidence. This would provide clarity on complex issues and help jurors navigate the case more effectively. It would be a practical, cost-effective step that maintains the integrity of jury trials, while addressing challenges specific to complex medical manslaughter and murder cases.

This medico-legal expert would serve solely to assist the jury in understanding complex issues presented during the trial, and would have no role in the deliberation or decision-making process. They are separate to the judge who oversees the trial, and their precise expertise would be dependent on the particular nature of the case.

Of course, everything would have to be confidential in accordance with jury rules – their introduction would simply be to facilitate decision-making and explain complex matters to the jury.

I believe it’s in the interests of both parties, the defendant and the prosecution, that the jury fully understands the evidence presented in court. An impartial medico-legal expert could help ensure this understanding, without influencing the case’s outcome. Their role would be beneficial for clarity, helping both parties ensure the jury comprehends the complex evidence before them.

Further, it may also be worth considering specialist medical juries for certain complex criminal cases, such as the Letby trial, where the evidence is highly technical. The sheer volume of complex medical information presented for each baby in this case suggests that a jury without specialised medical knowledge could struggle to fully grasp the evidence.

Appeals process

One of the Letby appeal grounds involved an application to admit fresh evidence from Lee, challenging the conclusions reached from the 1989 study he co-authored. The court of appeal denied this, noting it did not meet the standards for fresh evidence. Refusals such as this highlights an essential aspect of public debate: the need for transparency about how the court of appeal evaluates new evidence, especially in cases that receive significant media attention.

While it remains to be seen whether the court grants a new appeal for Letby, after the criminal cases review commission reviews the latest evidence provided by Lee’s panel, the Thirlwall inquiry has been sitting since September 2023, looking at events at the Countess of Chester Hospital on the basis that Letby is guilty. It will ultimately make recommendations about different aspects of this wider medical ecosystem, but it’s got no legal authority. Inquiries can make valuable recommendations, but they are advisory in nature and cannot enforce legal changes or compel action.

There are numerous other examples where criminal trials have not led to the systemic-level changes that they highlight are urgently needed, beyond the individual verdict. During the trial of Hadiza Bawa-Garba – a junior doctor found guilty of manslaughter in November 2015 on the grounds of gross negligence manslaughter following the death of a six-year-old boy in her care – it was revealed that the Leicester NHS trust’s serious incident report had identified 93 failures, only six of which were attributable to the doctor herself.

Ultimately, while holding individuals accountable is essential, we must also shift our focus towards long-term, systemic reform. Only by addressing the root causes and strengthening oversight within healthcare institutions can we ensure that tragedies are never repeated. The criminal justice system, though necessary in cases of clear criminal conduct, should be complemented by proactive, preventative measures that foster a culture of safety, accountability and transparency in healthcare.

To hear about new Insights articles, join the hundreds of thousands of people who value The Conversation’s evidence-based news. Subscribe to our newsletter.

Amel Alghrani does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

US Drug Enforcement Administration images accompanying a warning about the emergence of nitazenes in Washington DC, June 2022USDEA

In the early hours of September 14 2021, three men parked in a quiet car park in the southern English market town of Abingdon-on-Thames. The men, returning from a night out, had pulled over to smoke heroin.

Unknown to them, the drug had been fortified with a nitazene compound called isotonitazene, a highly potent new synthetic opioid. Two of the men, Peter Haslam and Adrian Davies, overdosed and went into cardiac arrest. The third, Michael Parsons, tried to save them and himself by injecting naloxone, an opioid overdose antidote. Despite paramedics also trying to resuscitate Haslam and Davies, both died at the scene.

Their deaths were among at least 27 fatalities linked to nitazenes that year in the UK. Since then, nitazenes – otherwise known as 2-benzylbenzimidazole opioids – have become more prevalent in the UK’s illegal drug supply, leading some experts to warn that they are a major new threat because of their extreme potency.

In June 2023, the UK’s most recent outbreak of deaths linked to synthetic opioids emerged in the West Midlands when drug dealers used nitazenes to fortify low-purity heroin. By August, there were 21 nitazene-related fatalities in Birmingham alone. In some cases, dealers also added xylazine (colloquially known as “tranq”), a non-opioid sedative used by vets.

The increasing availability of these and other synthetic drugs led the UK’s National Crime Agency (NCA) to warn in August 2024 that “there has never been a more dangerous time to take drugs”. Like Haslam and Davies, many heroin users are unaware they might also be consuming nitazenes, which significantly increase the risk of overdose.

Given their potency, only a small amount of nitazene is required to produce a fatal dose. While some studies have concluded that nitazenes are even more potent than the synthetic opioid fentanyl, which causes many thousands of deaths in the US, the NCA judges it a “realistic possibility” that the potency of both substances are “broadly equivalent” – making them roughly 50 times more potent than heroin.

Illicit drug use is damaging large parts of the world socially, politically and environmentally. Patterns of supply and demand are changing rapidly. In our new longform series Addicted, leading drug experts bring you the latest insights on drug use and production as we ask: is it time to declare a planetary emergency?

Officially, more than 400 deaths plus many non-fatal overdoses were linked to nitazenes in the UK between June 2023 and January 2025. But this is likely to be an underestimate because of gaps within forensic and toxicology reporting. These figures come amid record levels of drug-related deaths in England and Wales. In 2023, there were 5,448 deaths related to drug poisoning, an 11% increase on the previous year and the highest total since records began in 1993.

This is of particular concern given that the UK has the largest heroin market in Europe, comprising around 300,000 users in England alone. While nitazene-related deaths are still relatively low (although by no means insignificant) compared with those from heroin and other opioids, these new synthetic opioids are cheap and easy to buy, and offer dealers multiple advantages over traditional plant-based drugs.

Unlike opium, nitazenes and other synthetic opioids can be produced anywhere in the world using precursor chemicals that are often uncontrolled and widely available. Producer countries including China and India have not yet banned all nitazene compounds, meaning they are sold legally – mostly online. Chemical manufacturing companies in these countries can synthesise nitazenes at scale using a comparatively easy three or four-step process.

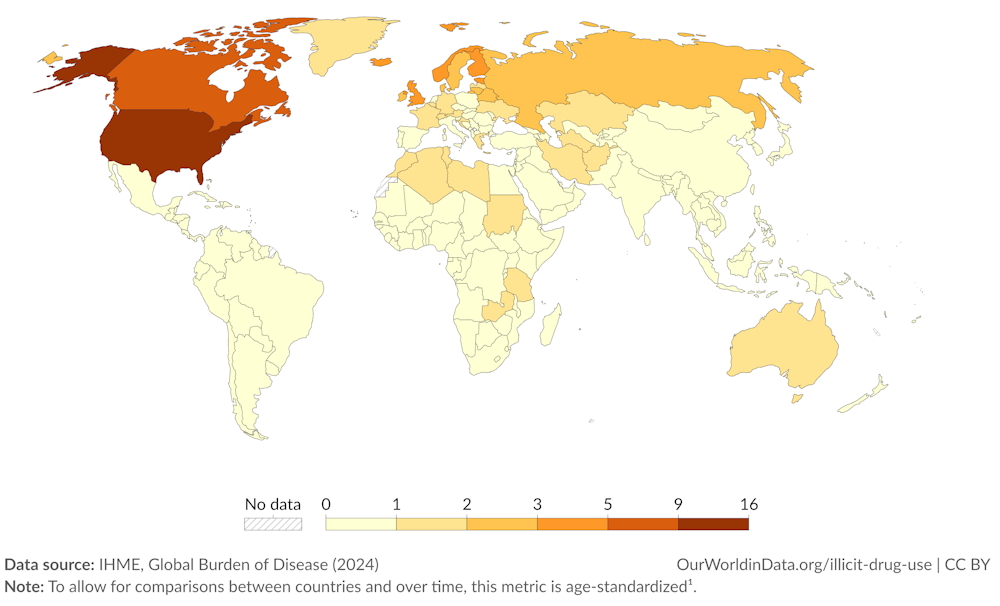

Opioid use death rates around the world:

Estimated deaths from opioid use disorders per 100,000 people in 2021. Our World In Data, CC BY

For the past 15 years, I have researched and advised on the international narcotics industry, especially the Afghan drug trade, as an academic, UK Home Office official and consultant. I’ve observed many shifts within global drug markets, and I believe the increasing availability of synthetic drugs in the UK and Europe may represent a new chapter in illicit drug use here – with the emergence of nitazenes only adding to these concerns.

A brief history of synthetic opioids

New synthetic opioids (NSOs) are one of the fastest-growing groups of new psychoactive substances around the world. The EU Drugs Agency (EUDA) currently monitors 81 NSOs – the fourth-largest group of drugs under observation.

NSOs largely fall into two broad groups: fentanyl and its analogues, and non-fentanyl-structured compounds – these include nitazenes, among many other substances.

Many of these “new” synthetic opioids have, in fact, existed for decades. Nitazenes were first synthesised in the 1950s by the Swiss pharmaceutical company, Ciba Aktiengesellschaft, as pain-relieving analgesics, although they were never approved for medical use.

Prior to 2019, there had only been limited reports of nitazenes in the illegal drug supply – including a “brownish looking powder” found in Italy in 1966; the discovery of a lab in Germany in 1987; several nitazene-related deaths in Moscow in 1998; and a US chemist illegally producing the drug for personal use in 2003. But since nitazenes re-emerged at the end of the last decade, over 20 variants have been discovered.

Paul Janssen, the Belgian chemist who first made fentanyl. Johnson & Johnson

The most common NSO in the illegal drug market, fentanyl, was first synthesised by Belgian chemist Paul Janssen in 1960. Fentanyl, which is roughly 100 times more potent than morphine, was approved in the US in 1968 for pharmaceutical use as an analgesic.

Over the next four decades, however, illegally produced fentanyl resulted in three relatively small outbreaks of deaths in the US. A fourth, larger fentanyl outbreak in Chicago, Detroit and Philadelphia resulted in about 1,000 deaths between 2005 and 2007.

The current US fentanyl crisis started in 2013, expanding to affect much of the country. Between 2014 and 2019, Chinese companies were the main manufacturers of finished fentanyl substances in the US – to combat this, both the Obama and Trump administrations lobbied Beijing to curtail the fentanyl industry.

The Chinese government responded by controlling specific fentanyl analogues. However, every time an analogue was banned, chemists there would slightly adjust the formula to produce a new compound that mirrored the banned substance.

China finally banned all fentanyl-related substances in May 2019, prompting two significant changes in the drug’s supply: a slowdown in the development of new fentanyl analogues, and a reduction in their direct sale to the US from China. Instead, Chinese companies increasingly sent fentanyl precursors to Mexican drug cartels who would synthesise fentanyl (or counterfeit medication) in clandestine labs, before smuggling it across the US border. Consequently, Mexico is now the primary source of fentanyl in the US.

But these supply changes led to another shift in the global drugs arena, as China’s chemical and pharmaceutical businesses – keen to develop new markets – adjusted their focus to producing uncontrolled synthetic substances, including nitazenes. At the same time, they expanded their geographical focus from North America to include Europe and the UK.

The nitazene supply chain

Producing nitazenes is a relatively low-cost exercise. They are largely manufactured in laboratories – both legal and illegal – in China, before being smuggled to the UK and Europe via fast parcel and post networks.

Nitazenes’ high potency means only small quantities are required, making them easier to transport and harder for border officials to detect. Some Chinese vendors have reportedly been offering to hide nitazenes in legitimate goods such as dog food and catering supplies, to circumvent custom controls. All of this decreases the risk to sellers, and lessens the price of doing business.

In March 2024, two China-based sellers operating on the dark web were selling a kilo of nitazene for between €10,000 and €17,000 (£12,000-£20,000). During roughly the same period, a kilo of heroin at the wholesale level in the UK was selling for between £23,000 and £26,000. Once bought, nitazenes are largely used to fortify low-purity heroin, although the drug can also be made into pills.

Video by The Guardian.

Nitazenes are not limited to the dark web. They are widely and openly advertised on the internet, social media and music streaming platforms. In February 2024, one China-based e-commerce site displayed 85 advertisements for nitazenes. Such sites also sell a range of other synthetic drugs, including fentanyl analogues and precursors, xylazines, cannabinoids and methamphetamine.

This means drug dealers in the UK and across the world no longer need to have established connections to underworld figures to source illegal drugs. With a click of a mouse, they can have them delivered to their home address. In this sense, the internet has democratised the drug trade by widening access beyond “traditional” criminals.

In the UK, while the supply of nitazenes is currently assessed as “low”, a number of smaller-scale organised crime groups are importing them to fortify low-purity heroin, before largely dealing it at the “county lines” level. This involves organised crime groups moving drugs – primarily heroin and crack cocaine – across towns, cities and county borders within the UK, using mobile phones or another form of “deal line” to sell to customers.

In November 2023, Leon Brown from West Bromwich was imprisoned for seven years for dealing drugs containing nitazenes – a verdict described as “a great result in our ongoing efforts to tackle county lines drug dealing” by detective sergeant Luke Papps of the South Worcestershire county lines team.

A few larger UK criminal networks have also been involved in nitazene distribution. In October 2023, the police and Border Force conducted raids across north London, arresting 11 people. They dismantled a drug processing site and seized 150,000 tablets containing nitazene – the UK’s largest ever seizure of synthetic opioids – as well as a pill-pressing machine, a firearm, more than £60,000 in cash and £8,000 in cryptocurrency. The police suspected the group had been selling the tablets on the dark web.

Anecdotal reports suggest there have been mixed reactions to the introduction of nitazenes into the illegal drug supply. Richard, a recovering heroin user from Bristol, told Vice magazine that, given their potency, some “people are scared of [nitazenes]” while others are “actively seeking” them.

As has been the case with fentanyl in the US, users build up tolerance and therefore seek stronger doses. Manny, a heroin user from Bristol, told Vice: “I smoked [heroin cut with nitazenes] and it felt like the first time I’d ever taken drugs.”

Video by Vice.

UK-based criminals also use the dark web to export nitazenes abroad. In October 2023, the Australian Border Force identified 22 nitazene discoveries in packages shipped to the country via mail cargo from the UK. British criminals have also trafficked counterfeit medicines containing nitazenes to Ireland and Norway.

Use of nitazenes is now being detected all over the world. Within Europe, Ireland experienced several nitazene outbreaks in 2023-24 while in Estonia, nitazenes now account for a large share of overdose deaths – a trend also seen (to a lesser extent) in Latvia. Preliminary data suggests at least 150 deaths were linked to nitazenes in Europe in 2023.

Nitazenes have also been discovered in fake pain medication such as benzodiazepines, oxycodone and diazepam, which widens the number of people at risk to include those with no opioid tolerance. The death in July 2023 of Alex Harpum, a 23-year-old British student who was preparing for a career as an opera singer, was a stark reminder of the danger of buying fake medicine online that may have been contaminated with nitazenes.

The nitazene ‘boom’ and the global heroin trade

For decades, Afghanistan was the world’s largest opium producer and the source of most of Europe’s heroin. Then in April 2022, the ruling Taliban announced a comprehensive prohibition on the use, trade, transport, production, import and export of all drugs. As a result, poppy cultivation has fallen to historically low levels for a second consecutive year.

While this has not, as yet, translated into a shortage of heroin on European streets, including in the UK and Germany, some indicators suggest a slowdown in heroin supplies to the UK. In the year March 2023-24, the quantity of heroin seized in the UK fell by 54%, from 950kg to 441kg. This is the lowest quantity of heroin seized since 1989, when about 350kg was intercepted.

The NCA assesses that the Taliban ban has created market “uncertainty”. The wholesale price of heroin has increased from roughly £16,000 per kilo prior to the COVID-19 pandemic to about £26,000, while anecdotal reports suggest average heroin purity for users dropped to under 30% (often to 10-20%) in 2024, compared with around 35% in 2023 and 45% in 2022.

Video by UN Story.

Even without the Taliban’s ban, heroin is not easy to produce and supply. Cultivating opium poppy is labour-intensive, taking five or six months. The static nature of opium fields means they are visible and susceptible to eradication; poppy crops can also be negatively affected by blight or drought.

Converting opium into heroin base is also a labour-intensive process that can involve (depending on the production method) at least 17 steps. Acetic anhydride, the main chemical used to convert morphine into heroin, is relatively expensive compared with synthetic precursors. Moreover, heroin is a bulky product, which means it is harder to move in large volumes.

While the relationship between events in opiate-producer countries and the introduction of synthetic opioids to consumer markets should not be overstated, this new type of drug offers economic advantages to criminals whose “sole motivation is greed”.

For decades, Turkish, Kurdish and Pakistani criminal networks have been responsible for importing heroin into the UK. Once in the UK, both Turkish and British groups largely control its wholesale supply, with some participation of Albanian gangs.

To date, there is little evidence to suggest these groups have transitioned to supplying NSOs, including nitazenes. The shifting dynamics in the global drug supply chain, however, could upend traditional markets and the gangs who profit from them.

America’s synthetic drug crisis

The synthetic opioid fentanyl has devastated the US, having been linked to about 75,000 deaths in 2023 alone. It is the primary cause of death for Americans aged 18-49. Canada, too, has experienced a wave of deaths: between January 2016 and June 2024, there were 49,105 apparent opioid deaths there, with fentanyl implicated in a large proportion.

More than 4,300 reports of nitazenes have reached the US National Forensic Laboratory Information System since 2019. They are typically used to fortify fentanyl and other opioids, which can produce a fatal concoction.

Efforts to stem the flow of NSOs, including nitazenes, from China to the US and elsewhere will prove challenging. And even if China does implement stricter controls, other countries could step in to fill the void. According to the Commission on Combating Synthetic Opioid Trafficking:

The overall sizes of these industries, limited oversight efforts and political incentives contribute to an atmosphere of impunity among firms and individuals associated with those industries.

While US and Chinese counter-narcotics cooperation ended in 2022 amid increasing geopolitical tensions, the following November’s summit in Woodside, California, between presidents Joe Biden and Xi Jinping saw them agree to recommence collaboration.

As a result, China recently closed several chemical companies that were shipping fentanyl precursors and nitazenes to the US. These vendors used encrypted platforms and cryptocurrency to conduct the deals, and mislabelled the consignments to try to ensure the substances evaded border controls. China has also outlawed more chemicals and substances, including several nitazene variants.

But President Trump’s imposition of tariffs on imports from China – which sit alongside proposed taxes on imports from Canada and Mexico, in part for supposedly not doing enough to curb the trafficking of fentanyl and its precursors to the US – threatens this counter-narcotics cooperation.

While nitazenes are not yet widely available in the US, their presence within some fentanyl batches is complicating the US opioid crisis – and according to some experts, has the potential to further increase the already shocking number of synthetic opioid-related deaths.

The UK response to nitazenes

Successive UK governments have made tackling NSOs a high priority. Shortly after the most recent nitazene-related deaths were discovered in the UK in summer 2023, the NCA launched Project Housebuilder to lead and coordinate the law enforcement and public health response.

This was soon followed by the establishment of a government-wide Synthetic Opioids Taskforce “to improve…understanding, preparedness and mitigation against this evolving threat”. Chris Philp, then the UK’s combatting drugs minister, stated that “synthetic opioids are at the top of [this government’s] list because of the harm they cause”.

The taskforce has taken a range of measures, such as controlling more NSOs as class A drugs, conducting more intelligence operations at UK borders, widening access to naloxone, and enhancing the UK’s real-time, multi-source drug surveillance system. The government also worked with the US and Canada to learn from their experiences.

Recently, the current UK government banned a further six synthetic opioids and introduced a generic definition of nitazenes as class A drugs. And the UK’s current government, unlike its Conservative predecessor, has also indicated its willingness to consider evidence from the UK’s first drug consumption facility, which recently opened in Glasgow.

Other policy measures worthy of consideration include expanding drug checking services whereby drug users submit drugs to a lab to test what is in them, then are provided with information about the sample. These services offer vital information to the public and authorities about current drug trends.

While there is high uncertainty about what is going to happen next in the UK regarding illicit drug trends, the evolution of the US drug landscape over generations provides some important lessons.

Lessons from the US

The US fentanyl crisis shows drug markets can change quickly with long-lasting consequences. Most heroin on US streets contains – or has been replaced by – fentanyl. According to DEA seizure data, US heroin seizures declined by nearly 70% between 2019 and 2023, whereas fentanyl seizures have increased by 451%.

However, illegal drug markets evolve in different ways and at different paces. In May 1989, Douglas Hogg, a UK Home Office minister, travelled to the US and the Bahamas on a fact-finding mission about crack cocaine, a drug that was predicted to spread from the US to the UK. Upon his return, Hogg noted:

The ethnic, social and economic characters of many of our big cities are very similar to those in the US. If they have a crack problem, why should not we? … The use of crack in Great Britain is likely to develop very substantially over the next few years.

But this “crack invasion”, as some called it, did not materialise in the UK to the extent it had in the US – and the same was true about a predicted wave of methamphetamine use in the UK, which remains low compared with the US.

It is also unlikely the UK and Europe will experience a synthetic opioid crisis on the same scale as the US. The first wave of the US crisis was driven by extensive overprescription of opioids for pain relief. This increased the number of people addicted to opioids, some of whom later turned to heroin, before transitioning to fentanyl. In contrast, large-scale opioid prescriptions have not been a major issue in the UK or Europe, although there is some diversion of legal fentanyl into the illegal drug market in Europe.

Video by The Brookings Institution.

According to Alex Stevens, professor of criminology at the University of Sheffield, another factor differentiating the US and Europe is the provision of drug treatment and harm reduction programmes. Opioid users in Europe, and to a lesser extent in the UK, are much more likely to be in medication-assisted treatment than their US counterparts, thus reducing the number of people at risk. These interventions are reinforced by different socioeconomic factors in much of Europe, such as lower economic inequality, stronger social protections, and better healthcare systems.

None of this, though, means the nitazene threat in the UK and Europe should be underestimated, nor that use and supply of these drugs (and other NSOs) will not increase from its current relatively low base. As the NCA recently warned:

While a zero-tolerance approach from law enforcement, plus advice to users on the heightened dangers, may contain or slow the current uptake, we must prepare for these substances to become widely available, both unadvertised in fortified mixes and in response to user demand as a more potent high.

The future of new synthetic opioids

Predicting the future of NSO use and trafficking is a challenging task. Projections for Europe range from existing opiate stockpiles ensuring that heroin consumer markets remain serviced (assuming the Taliban ban is short-lived), to a heroin shortage which results in more drug dealers turning to NSOs to plug the shortfall, which in turn could lead to lasting changes in European drug markets (as happened in a few countries following the Taliban’s first opium ban in 2000-01).

In such a scenario, it is possible that Turkish criminal networks may exploit their links with Mexico’s Sinaloa cartel to source NSOs. Mexican criminal gangs also operate in Europe, which may increase the likelihood of them trying to open a new NSO market on the continent.

There is also evidence that some Italian criminal organisations have entered the NSO marketplace. In November 2023, Italian authorities announced the seizure of 100,000 doses of synthetic drugs, including fentanyl, as part of operation Painkiller, a joint Italian-American initiative.

Given the many advantages for criminal groups of NSOs, it seems likely they are here to stay. A key question is whether nitazenes (or other NSOs) will supplant traditional heroin as the opioid of choice, as they have done in the US, or remain at relatively low levels in Europe, co-existing with or mixed into the heroin supply.

In December 2023, Paul Griffiths, the EUDA’s scientific director, told Vice: “We’re not seeing much new initiation of heroin use in Europe. So in five to ten years … as heroin users get older and more vulnerable, we’re not going to have much of an opiate problem left.”

But he warned that if heroin use does dry up: “You might then see opioids appearing in other forms and preparations, such as pills, that could potentially become popular among younger age groups who currently do not appear attracted to injecting heroin.”

While previous NSO outbreaks in the UK were relatively short-lived and limited in scale, the most recent nitazene outbreak, which started in summer of 2023, has been more sustained, covered more parts of the UK, and involved more fatalities. The broader trend in Europe also suggests the prevalence and variations of NSOs are increasing at a faster pace than in previous years.

Notwithstanding, nitazene use and supply in the UK currently remains relatively low. In fact, the rate of nitazene-linked deaths – at least those officially reported – decreased between spring 2024 and the end of the year.

In the short term, then, it seems unlikely there will be a nitazene “explosion”. Rather, criminal groups will probably try to increasingly embed nitazenes into the UK drug market at a similar pace to the last 18 months.

However, this situation could change rapidly in future, especially if larger criminal networks involved in heroin importation switch to smuggling NSOs, and there is a genuine shortage of Afghan heroin. This problem would be compounded if drug users start seeking nitazenes, thus creating demand for them.

Either way, the UK government, along with its European partners, should continue to reinforce the whole drug system, to prepare for the worst-case scenario.

To hear about new Insights articles, join the hundreds of thousands of people who value The Conversation’s evidence-based news. Subscribe to our newsletter.

Philip A. Berry does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

Donald Trump has hit the 30-day pause button on imposing 25% tariffs on Canada and Mexico, but is proceeding with slapping 10% tariffs on Chinese imports, and tariffs on the EU are still on his agenda.

Trump has declared that “tariff” is “the most beautiful word in the dictionary”. Yet as the president weighs up the sweeping consequences of his tariff fixation, he may want to throw out the dictionary and pick up a history book.

The magnitude and scale of the proposed tariffs hark back to the US Smoot-Hawley Tariff Act enacted in 1930.

For example, Nobel Laureate economist Paul Krugman told Bloomberg that “we’re really talking about tariffs on a scale that we … have not seen,” adding that “we’re talking about a reversal of really 90 years of US policy”.

The Smoot-Hawley tariffs were initially intended to provide support to the deeply indebted US agricultural sector at the end of the 1920s, and protect them from foreign competition – all familiar themes to the anti-free-trade rhetoric peddled by Trumpists today.

The advent of the Great Depression had generated widespread, albeit not universal, demands for protection from imports, and Smoot-Hawley increased already significant tariffs on overseas goods. Members of Congress were eager to provide protection, trading votes in exchange for support for their constituents’ industries.

Although at the time more than 1,000 economists implored President Herbert Hoover to veto Smoot-Hawley, the bill was signed into law. The resulting tariff act led to taxes averaging nearly 40% on 20,000 or so different types of imported goods.

The history of trade tariffs in the US.

The culmination led to a dramatic decline in US trade with other countries, particularly among those that retaliated, and is widely acknowledge as severely worsening the Great Depression. According to one estimate, the sum of US imports plummeted by nearly half.

What’s more, the impacts were felt globally. Protectionist policies are believed to have accounted for about half of the 25% decline in world trade, and indirectly helped create economic factors that led to the second world war.

The blowback against Capitol Hill was immense as well: the optics of vote trading over the tariff act resulted in Congress delegating control over trade policy to the president just four years later because the behaviour was regarded as so reckless.

All of this came against the backdrop of diplomatic American isolationism in the 1930s, which were not unlike many of Trump’s current efforts to retreat from – or even attack – multilateral institutions.

Despite President Woodrow Wilson winning the Nobel Peace Prize in 1919 for his work initiating the League of Nations (a forerunner of the United Nations), for example, the US never became a member. The term “America first” was also used widely in this period to refer to a focus on domestic policy and high tariffs.

Fast forward to present day

Trump has said that his tariffs will cause “some pain” but are “worth the price that must be paid.” Based on recent estimates from the non-partisan Peterson Institute for International Economics, Trump’s tariffs could drive up costs for the average US household more than US$1,200 (£963) per year.

Whether US voters will still stand behind Trump when actual prices begin to rise is still to be determined.

However, many Republicans on Capitol Hill have rushed to Trump’s defence. Congresswoman Claudia Tenney of New York told Fox News that she’s glad the US is “projecting strength for once on the world stage”. Senator Eric Schmitt of Missouri insisted that tariffs were “not a surprise,” emphasising that Trump had relentlessly campaigned on “improving our standing in the world.”

Perhaps the sharpest Republican rebuke came from Sen. Mitch McConnell of Kentucky, who labelled the tariffs simply a “bad idea”.

Public opinion data show that tariffs are hotly contested, with partisanship shaping both general views toward tariffs and views on specific national targets.

According to a January 2025 Harvard CAPS/Harris poll, 52% of Americans overall approve of placing new tariffs on China, with 74% of Republicans in favour, but just 34% of Democrats.

Support is more modest for imposing tariffs on America’s neighbours. Only 40% of voters think tariffs on Canada and Mexico are a good idea, including 59% of Republicans and 24% of Democrats.

Tariffs rank low on a list of national priorities. A mere 3% of Americans think tariffs on Canada and Mexico should be a top priority for Trump in his first 100 days, while just 11% rank tariffs on China as a top priority.

Prospect of a broader trade war

What seems clear is that Trump’s proposed tariffs against Canada, Mexico, and China could be just the opening salvos in a broader tit-for-tat that may extend to Europe, and beyond.

At home, the political challenge for Trump is to keep intact what increasingly looks like a fragile coalition – balancing the interests of hardline Maga supporters who reject free trade and tech titans who see tariffs as disrupting vital supply chains, especially to Asia.

After Trump’s election, former adviser and populist nationalist Steve Bannon warned that America would no longer be “abused” by “unbalanced trade deals.” “Yes, tariffs are coming,” he said. “You will have to pay to have access to the US market. It is no longer free, the free market is over.”

Meanwhile, Silicon Valley has been mostly silent on the tariffs. While tech moguls are doubtlessly trying to curry favour for tariff exemptions or the reduction of tariffs altogether, it’s possible that they have been assured that the tariffs are about leverage and will be gone soon enough.

Regardless, Trump is showing that tariffs are a crucial part of his “America first” foreign policy, a kind of belligerent unilateralism that treats allies and adversaries alike as pieces to be moved around a chessboard.

Under Trump, the “art of the deal” means throwing America’s weight around as the world’s economic superpower, and waiting for the leaders of other nations to fold. Whether American voters will endure the economic costs necessary for his plans could determine his resolve.

Trump may think that tariff is a beautiful word now. But if even a glimmer of the 1930s repeats itself, its economic shadow could soon look grim.

The authors do not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and have disclosed no relevant affiliations beyond their academic appointment.

Source: United Kingdom – Executive Government & Departments

Scientists comment on the Public Accounts Committee (PAC) report on Carbon Capture, Usage and Storage (CCUS) technologies.

Prof Hannah Chalmers, Personal Chair of Sustainable Energy Systems, Institute for Energy Systems, School of Engineering, University of Edinburgh, said:

“CCUS technologies can play a unique role in tackling carbon dioxide emissions. They can be used at large industrial sites to ensure that most of the carbon dioxide produced by activities like iron and steel production is not emitted to the atmosphere. Instead, the carbon dioxide is permanently stored in geological formations (rocks). In the UK, CCUS projects are developing plans to store carbon dioxide in layers of rock that are deep underneath the sea.

“There is also ongoing work to develop and deploy cost-effective approaches to remove carbon dioxide directly from the air. This provides an important option to respond to the widely reported increases in carbon dioxide levels in the atmosphere that are causing significant concern.

“There is significant evidence that including CCUS in a mix of technologies to reduce carbon dioxide emissions will be the most cost-effective way to address climate change. Several large-scale projects have been operating in other countries for many years. Experience from these projects is being used to ensure that the CCUS projects that are being developed in the UK are designed to be reliable and cost-effective.”

Dr Stuart Gilfillan, Reader in Geochemistry, University of Edinburgh, said:

What is CCUS technology, how does it work, does it have limitations?

“CCUS stands for Carbon Capture, Utilisation, and Storage, which is a developing technology which reduces the amount of carbon dioxide (CO2) released into the atmosphere. It works by capturing CO2 at the point source, transporting it and then burying it for safe storage in rocks over a kilometre below the ground surface. Like any technology, it has pros and cons, and costs more than simply releasing the CO2 directly to the atmosphere, which is currently free. CCUS is the only currently available technology that can directly reduce CO2 emissions from sources like power plants and industrial processes. Given that global temperature records are now being broken on an almost daily basis and yesterday’s announcement of the hottest January on record, it is essential tool in the urgent fight against runaway climate change.

What is the existing evidence around the efficacy of CCUS?

“CO2 capture technology has proven successful in capturing up to 90-95% of CO2 emissions from point of sources from power stations and industrial facilities. Successful examples include the Boundary Dam power station in Saskatchewan, Canada, where a large-scale CCUS unit has been operational since 2014, capturing about 1 million tonnes of CO2 per year.

“The long-term storage of CO2 is proven by natural CO2 reservoirs around the world and engineered projects like Sleipner in the North Sea, which have been injecting CO2 beneath the seabed since 1996 without significant issues. Research over the past two decades has developed monitoring technologies that can detect and mitigate potential leakage and to ensure that CO2 remains securely buried in rocks deep underground.

What more evidence may be needed to be confident in its applications?

“No more evidence is required, as exemplified by the UK’s Climate Change Committee (CCC), which is an independent body established under the Climate Change Act who advise the government on emissions targets and report to Parliament on progress made in reducing greenhouse gas emissions. The CCC is clear that CCUS is a critical technology for the decarbonisation of the UK economy, particularly in sectors that are hard to decarbonize directly, such as heavy industry (steel, cement, chemicals) and power generation.

“CCUS is not only as a standalone technology but is an essential part of a broader strategy to reach net-zero emissions by 2050. It compliments energy efficiency, renewable energy deployment, and electrification. CCUS is a clear driver for regional economic development, particularly in regions with suitable geological storage sites and industrial bases, such as the East Coast of Scotland, the Humber region, and North East England, areas that have been ‘left behind’ in recent times.”

Dr Tim Dixon, IEA Greenhouse Gas, Director and General Manager, said:

“Carbon Capture and Storage (CCS) is a necessary technology for the UK and other countries to achieve net-zero, and we need all low-carbon energy technologies. The science case for the role of CCS is provided by the UK’s Climate Change Committee, the Intergovernmental Panel on Climate Change (IPCC) and the International Energy Agency (IEA) and cannot be disputed if climate change is to be taken seriously. The key aspect of CCS is the secure long-term retention of CO2 in deep geological formations, and we have decades of experience in this from around the world. With over 40 large scale projects in operation injecting millions of tonnes every year and many pilot-scale projects, this has allowed us to test the science, the monitoring and the practicalities of geological storage of CO2. Hence CO2 geological storage is a proven technology and the regulations to enable and to ensure that it is safe and secure are based upon this sound science and experience. ”

Professor Paul Fennell FIchemE, Professor of Clean Energy, Imperial College London, said:

“The idea that Carbon Capture and Storage is an unproven technology is simply untrue. There are projects ongoing around the world, and millions of tonnes of CO2 have been safely stored over the last couple of decades. This has not happened in the U.K. because of our sclerotic inability to develop public infrastructure, not because the technology is unproven.”

Dr Greg Mutch, Researcher in Carbon Capture and Storage, Newcastle University, said:

“Carbon capture and storage is a technology that prevents carbon dioxide from entering the atmosphere, by capturing it and storing it underground in ‘empty’ oil & gas reservoirs or saline aquifers. According to the world’s foremost experts on the subject, gathered to contribute the International Panel on Climate Change, carbon capture and storage processes are necessary to achieve climate change mitigation goals at lowest cost. Without scalable CCS technologies by the end of the century, climate change mitigation will cost between 29 and 297% (mean value 138%) more.[1] Moreover, CCS is predicted to provide tens of thousands of jobs in the UK, add several billion pounds in terms of gross value added per year by 2050,[2] and enable other important technologies (hydrogen production etc) that will come with further jobs and economic value.”

[1] IPCC, 2018: Global Warming of 1.5 °C. An IPCC Special Report on the impacts of global warming of 1.5 °C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty, ed. V. Masson-Delmotte, P. Zhai, H.-O. Portner, D. Roberts, J. Skea, P. R. Shukla, A. Pirani, W. Moufouma-Okia, C. Pean, R. Pidcock, S. Connors, J. B. R. Matthews, Y. Chen, X. Zhou, M. I. Gomis, E. Lonnoy, T. Maycock, M. Tignor and T. Waterfield, Cambridge University Press, 2018.

[2] Energy Innovation Needs Assessment Sub-theme report: Carbon capture, utilisation, and storage, Vivid Economics, Carbon Trust, E4tech, Imperial College London, Frazer-Nash Consultancy, Energy Systems Catapult. Commissioned by the Department for Business, Energy & Industrial Strategy, 2019.

Professor Peter Styring, Director of the UK Centre for Carbon Dioxide Utilization, Professor of Chemical Engineering & Chemistry, University of Sheffield, said:

What is CCUS technology, how does it work, does it have limitations?

“CCUS is carbon capture and storage. This has been primarily focused on CCS as the main driver. It aims to capture carbon dioxide from emitters such as power stations and industries. The current technology temperature swing absorption (TSA) using a chemical reaction with an aqueous amine solvent to capture the CO2 from the mixed waste gas and then to release it in a purified form by increased temperature chemical desorption and then further drying and purification to get a gas that can be in theory transported to a site where the gas can be stored underground. It works but at a high energy cost and the production of amine decomposition products that need to be removed and more amine added. It costs a lot!

“Limitations are the energy and financial costs, permitting regulations on solvent disclosure and the large physical footprint. Full system lifecycle analysis is required but this is not always reported.”

What is the existing evidence around the efficacy of CCUS?

“This is not proven using current technologies. The problem is that the current government funded projects use old technologies to achieve CCS and what is actually needed is a step change to new, lower cost more efficient processes such as solid based pressure swing adsorption (PSA). The whole system tends to be simpler and the energy costs and land use is significantly reduced.”

What more evidence may be needed to be confident in its applications?

“Full evaluation of new technologies and rapid acceleration from proof of concept to capture at scale. The Innovate UK funded Flue2Chem project is a good example of how this is being addressed using mid-TRL technologies. The UK also needs to move away from a single minded storage approach to adding value through the use of CO2 in the production of chemicals that would otherwise be sourced from virgin fossil carbon. SUSTAIN project is making synthetic fuels from captured CO2 and Flue2Chem is making FMCG components, including surfactants and precursors from the CO2.”

Dr Stuart Jenkins, Net Zero Fossil Fuel Fellow, University of Oxford, said:

“The Public Accounts Committee are wrong to have labelled CCUS as ‘unproven’, there are many commercial scale projects around the world, but they are right to question the current model for funding it. We need to make sure the CCUS industry becomes self-sustaining, without the need for major taxpayer funding. One option — asking fossil fuel suppliers to contribute to these costs via a carbon storage mandate — is a fair and responsible approach going forward.

In a recent report we published working with researchers at the University of Oxford and Carbon Balance Initiative [1] we looked at the use of Carbon Storage Mandates, which place an obligation on fossil fuel producers to capture and store a rising fraction of the CO2 they produce, to support the UK’s CCUS industry.

Carbon storage mandates, in tandem with carbon pricing and other mechanisms, could deliver subsidy-free CCUS to the UK and provide investment certainty for companies.”

Dr Stuart Jenkins Our report was funded by the Carbon Capture and Storage Association, and consulted regulators, fossil fuel companies, capture and storage entities, UK Government, and academics on models for CCUS sector support packages.

Professor Paul Fennell: No conflicts other than being involved in CCs research.

Dr Tim Dixon: “Tim is a Director of IEA Environmental Projects Ltd (UK), a Non-Executive Director on the Board for The International CCS Knowledge Centre (Canada). He is also proud to be an Honorary Senior Research Fellow at the Bureau of Economic Geology, University of Texas in Austin, and an Honorary Lecturer at the School of Geosciences at University of Edinburgh. He was an original Board Member of the UK CCS Research Centre. Previously he worked in CCS, emissions trading, clean energy technologies and related areas for AEA Technology (ETSU), for the UK Government‘s Department of Trade and Industry (DTI) and for the Global CCS Institute. He was the EU’s Lead Negotiator for getting CCS in the CDM in UNFCCC in 2011, and a UK negotiator for getting CCS in the London Convention 2004-7, in OSPAR 2006-7, in the EU Emission Trading Scheme 2004-8, and inputting to the EU CCS Directive 2007-8. He gives talks on climate and CCS to schools and public organisations and supported the start of Oxford Climate Society at the University of Oxford. He is a Fellow of the UK Energy Institute, and member of the UK Institute of Physics and the UK Environmental Law Association.”

Dr Stuart Gilfillan “I have received funding from TotalEnergies in the past, for research related to CO2 origins in the subsurface and reservoir connectivity and Equinor on CO2 dissolution in natural CO2 reservoirs. I currently receive funding from the Natural Environment Research Council and Carbfix on CO2 mineralisation.”

Prof Hannah Chalmers “I work collaboratively with industrial partners who are developing CCUS projects in the UK (e.g. as a member of the Advisory Board for the Industrial Decarbonisation Research and Innovation Centre). I currently receive no funding from industry, but have received funding from industrial partners who are actively developing CCUS projects in the UK in the past (e.g. SSE plc).”

Professor Peter Styring: Peter is Professor of Chemical Engineering and Chemistry at the University of Sheffield (an investigator on Flue2Chem and SUSTAIN) and a Co-founder and Director of CCU International.

For all other experts, no response to our request for DOIs was received.

Premier Scott Moe will travel to Washington D.C. this week for meetings with U.S. elected representatives, industry organizations and to participate in the premier’s Council of the Federation (COF) joint-mission to Washington.

Prior to the COF mission, Premier Moe will meet with U.S. elected representatives and businesses to emphasize the strong trade relationship between Canada and the U.S, and the role Saskatchewan plays in supplying the continent with energy and food security.

“It’s important in the current economic environment that we engage with our counterparts in the United States to emphasize the shared benefit of trade between our two countries and turn the conversation toward building on those strengths rather than jeopardizing them with tariffs,” said Moe.

The U.S. is Saskatchewan’s largest and most important trading partner. About $40 billion worth of imports and exports cross the border every year. The current tariff-free border allows businesses to add value to products and economies, whether flowing from north to south or vice versa.

Premier Moe’s meetings will focus on maintaining strong Canada-U.S. relations by addressing shared issues such as the economy, energy, supply chains and the impacts of the Trump Administration’s proposed tariffs.

Premier Moe will also express Saskatchewan’s support for strong measures to secure the Canada-U.S. border.

“Strengthening border security and preventing the flow of illicit drugs like Fentanyl is a concern that has been identified by the U.S. and one that I share,” Moe added. “We are already taking action as a province through our Border Security Plan to ensure we have more officers and law enforcement presence at the Saskatchewan-U.S. border.”

The Council of the Federation’s joint-mission to Washington will allow all thirteen premiers to present a united voice on the important benefits that free-trade brings to Canada and the U.S. and the concern over the negative impact of tariffs to consumers and businesses on both sides of the border.

The COF program will take place on Feb 12 and will include meetings with U.S. elected representatives, business leaders and the Canada American Business Council.

Following the COF mission Premier Moe will travel to Mexico to engage with business and elected officials to advance relationships with this key trading partner.

Over the course of the next few weeks, Premier Moe and multiple cabinet Ministers will be travelling within Canada and beyond to advocate for Saskatchewan’s interests. These engagement efforts will focus on promoting the province as a global supplier of food and energy security, while strengthening relationships with our key international trading partners.

CALGARY, Alberta, Feb. 07, 2025 (GLOBE NEWSWIRE) — Canoe Financial LP (“Canoe Financial”) is recognized with three 2024 FundGrade A+® Awards for outstanding performance.

Canoe Financial 2024 FundGrade A+ Award winning funds:

FundGrade calculation date 12/31/2024.

The FundGrade A+® rating recognizes the best performing funds that deliver the most consistent risk-adjusted returns. It is a yearly award that honours the “best of the best” among Canadian investment funds that have maintained a high FundGrade rating throughout a calendar year.

“These awards are a testament to the strength of our investment philosophy and the dedication of our team. At Canoe Financial, we’re committed to helping Canadians build lasting wealth through disciplined, active management and a focus on delivering consistent, long-term performance,” said Darcy Hulston, President and Chief Executive Officer, Canoe Financial.

About Canoe Financial Canoe Financial is one of Canada’s fastest growing independent mutual fund companies managing $20 billion in assets across a diversified range of award-winning investment solutions. Founded in 2008, Canoe Financial is an employee-owned investment management firm focused on building financial wealth for Canadians. Canoe Financial has a significant presence across Canada, including offices in Calgary, Toronto and Montreal.

About FundGrade A+ Awards FundGrade A+® is used with permission from Fundata Canada Inc., all rights reserved. The annual FundGrade A+® Awards are presented by Fundata Canada Inc. to recognize the “best of the best” among Canadian investment funds. The FundGrade A+® calculation is supplemental to the monthly FundGrade ratings and is calculated at the end of each calendar year. The FundGrade rating system evaluates funds based on their risk-adjusted performance, measured by Sharpe Ratio, Sortino Ratio, and Information Ratio. The score for each ratio is calculated individually, covering all time periods from 2 to 10 years. The scores are then weighted equally in calculating a monthly FundGrade. The top 10% of funds earn an A Grade; the next 20% of funds earn a B Grade; the next 40% of funds earn a C Grade; the next 20% of funds receive a D Grade; and the lowest 10% of funds receive an E Grade. To be eligible, a fund must have received a FundGrade rating every month in the previous year. The FundGrade A+® uses a GPA-style calculation, where each monthly FundGrade from “A” to “E” receives a score from 4 to 0, respectively. A fund’s average score for the year determines its GPA. Any fund with a GPA of 3.5 or greater is awarded a FundGrade A+® Award. For more information, see www.FundGradeAwards.com. Although Fundata makes every effort to ensure the accuracy and reliability of the data contained herein, the accuracy is not guaranteed by Fundata.

Canoe Equity Portfolio Class Series, Canadian Focused Equity category out of a total of 70 funds: 20.20% (1 year), 9.46% (3 years), 14.48% (5 years), 10.16% (10 years) and 8.02% (since inception-February 2011); Canoe Asset Allocation Portfolio Class, Tactical Balanced category out of a total of 56 funds: 14.65% (1 year), 6.35% (3 years), 10.46% (5 years), 7.36% (10 years) and 5.85% (since inception-February 2011); Canoe North American Monthly Income Portfolio Class, Global Neutral Balanced category out of a total of 224 funds: 13.40% (1 year), 6.22% (3 years), 8.25% (5 years), 6.47% (10 years) and 7.25% (since inception- December 2012).

Further information Investor Relations Canoe Financial LP 1–877–434–2796 info@canoefinancial.com

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.

The Department of Finance and the Bank of Canada, in its role as the Government of Canada’s fiscal agent, are announcing the launch of securities lending of the government’s Canada Mortgage Bond (CMB) holdings, to support market well-functioning.

The government is making its CMB holdings available to borrow via CIBC Mellon/BNY’s pre-existing securities lending services, which uses a market-based pricing structure. CIBC Mellon/BNY was selected as agent based on a detailed evaluation of short-listed securities lending agents in the Canadian fixed-income market.

CMBs will be made available to borrow beginning Monday, February 10, 2025. The government is making its full holdings of CMBs available, and the daily average amounts on loan over the prior month for each security will be published on the Bank’s website by the fifth business day of the following month.

For further details, including terms and conditions, loan pricing, eligible collateral and to register as an eligible counterparty, please contact CIBC Mellon/BNY directly.

Note that as previously announced, the government will participate in all fixed-rate CMB syndications proposed for 2025 and will continue to target a total purchase amount of 50% of fixed-rate CMB primary issuances. The Bank of Canada will continue to conduct CMB purchases on the government’s behalf.

For further information, please contact:

Director Funds Management Division Department of Finance Canada 343‑549‑3651

Director Financial Markets Department Bank of Canada

Premier Tim Houston will join other Canadian premiers as part of the Council of the Federation mission to Washington, D.C., next week.

The delegation of 13 premiers will meet with U.S. political and business leaders to remind them of how both countries significantly benefit from free trade.

“I’m proud to stand in solidarity with my provincial and territorial colleagues and remind our American friends and allies that our economies thrive when we work together,” said Premier Houston. “We know the stakes are high – not just for Canadians and Nova Scotians but also for Americans who will also pay the price if tariffs are imposed.”

Premier Houston has a full schedule of meetings and events February 11-12. In addition to discussing the importance of stabilizing North America’s partnership, the premiers will also continue discussions on removing interprovincial trade barriers, improving labour mobility and diversifying markets.

Quick Facts:

Canada is the top export destination for more than half of all goods produced in the United States

motor vehicles, machinery, metals, minerals and agri-food made up more than 50 per cent of U.S. exports to Canada in 2023

in 2023, Nova Scotia exports to the U.S. were worth $4.4 billion and imports were $682.7 million

the goods with the largest volume shipped to the U.S. were tires, fish and prepared seafood, forest products and plastics

mission delegates are Premier Houston; Nicole LaFosse Parker, Chief of Staff and General Counsel; and Executive Deputy Minister Tracey Taweel

Baie Verte RCMP is investigating a fire that occurred yesterday, February 6, 2025, in Seal Cove that damaged a number of residential structures.

Shortly after 1:00 p.m. on Thursday, Baie Verte RCMP received a report of a residential fire on Newtown Road in Seal Cove. The fire, which is believed to have started in a residential shed, spread onto a number of other structures, including two other sheds and four houses. Two of these homes and three of the sheds were destroyed by fire. The remaining two homes were damaged. No one was injured.

The cause of the fire remains under investigation at this time.

Baie Verte RCMP is investigating a fire that occurred yesterday, February 6, 2025, in Seal Cove that damaged a number of residential structures.

Shortly after 1:00 p.m. on Thursday, Baie Verte RCMP received a report of a residential fire on Newtown Road in Seal Cove. The fire, which is believed to have started in a residential shed, spread onto a number of other structures, including two other sheds and four houses. Two of these homes and three of the sheds were destroyed by fire. The remaining two homes were damaged. No one was injured.

The cause of the fire remains under investigation at this time.

Green MP and party co-leader Adrian Ramsay has urged the government to divert planned new subsidies for the privately owned wood-burning Drax power station to a national home insulation scheme.

Adrian Ramsay said:

“Drax is a green energy scam, burning trees – some imported from ancient forests from as far away as Canada – subsidised by the taxpayer.

“The billions of pounds worth of subsidies run out in 2027, but the government is expected to try to renew them next week, turning taxpayer money into profits for a private company, instead of using the money to fuel a green energy revolution.

“Drax has benefitted from over £6 billion in subsidies since 2012 and neither taxpayers nor the environment can afford a penny more.

“The money should be used to help fund a national scheme of home insulation that would cut people’s energy bills and help to reduce energy use.

“Green MPs and Peers will be pressing the government to end this subsidy scandal and invest people’s money where it will make a real difference to them.”

SINGAPORE, Feb. 07, 2025 (GLOBE NEWSWIRE) — With the price of bitcoin once again trading below $100,000, many analysts believe it will enter a long period of high volatility. Holding spot positions may not continue to generate profits in the short term. BexBack Exchange is stepping up its efforts to provide traders with irresistible preferential packages. The platform now offers a 100% deposit bonus, a $50 welcome bonus for new users, and a 100x leverage on cryptocurrency trading, creating unparalleled opportunities for investors.

What Is 100x Leverage and How Does It Work?